Guide to taxation

Welcome to Farmers Weekly’s tax guide.

The tables show some of the main tax rates relevant to farmers and landowners in 20112/13. These have been provided by independent chartered accountant Saffery Champness.

Click on one of the headings below to find out more:

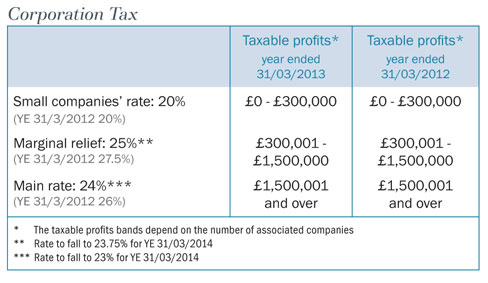

Corporation Tax

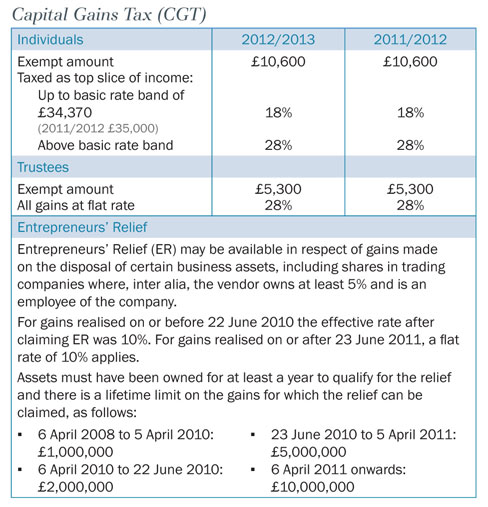

Capital Gains Tax

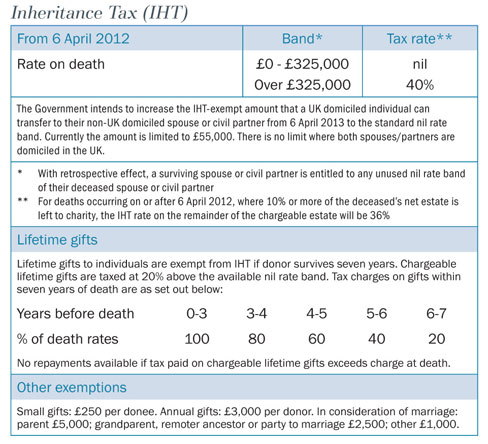

Inheritance Tax

Value Added Tax

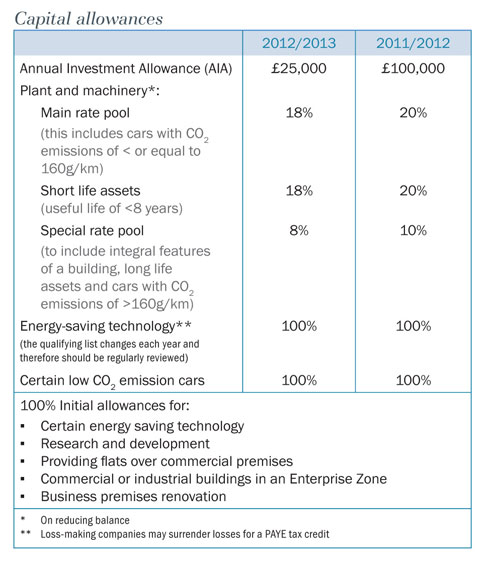

Capital allowances

Corporation Tax

Corporation Tax is a tax on the taxable profits of limited companies including farm businesses. Taxable profits for Corporation Tax include the profits from trading and investment profits – except dividend income which is taxed differently. If your farming company is subject to Corporation Tax you must inform HM Revenue & Customs (HMRC) that it’s liable for Corporation Tax, and you must pay the right amount of Corporation Tax on time and file a Company Tax Return and supporting documents There are different deadlines for each of these requirements. If you don’t meet those deadlines, your company may be charged interest and penalties.

Capital Gains Tax

Capital Gains Tax is a tax on the profit or gain you make when you sell or “dispose of” an asset. You usually dispose of an asset when you cease to own it – for example if you: sell it, give it away as a gift, transfer it to someone else, exchange it for something else, receive compensation for it e.g. you receive an insurance payout when an asset’s been destroyed. It’s the gain you make – not the amount of money you receive for the asset – that’s taxed. Most assets are liable to Capital Gains Tax when you sell or dispose of them – whether they’re in the UK or overseas. However, some assets are exempt, such as your car, personal possessions disposed of for £6,000 or less and, usually, your main home.

Inheritance Tax

Inheritance Tax is usually paid on an estate when somebody dies. It’s also sometimes payable on trusts or gifts made during someone’s lifetime. Most estates don’t have to pay Inheritance Tax because they’re valued at less than the threshold (£325,000 in 2010-11). However, most farms and rural estates will be in excess of this threshold. However, if you own a working farm, you can pass on some of your property free of Inheritance Tax in your will or before you die. You can claim relief for farm property such as farmland. You can also claim relief for farm buildings if the size of the buildings is proportionate to the size of the farming activity. If you are a landlord of farmland, it will normally qualify for relief of 100 per cent. However, property rented out under an agreement that commenced before 1 September 1995 usually only qualifies for relief of 50 per cent.

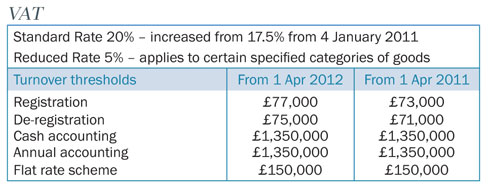

VAT

Value Added Tax (VAT) is a tax that’s charged on most goods and services that VAT-registered businesses provide in the UK. Farmers generally are able to recover all the VAT they incur on business purchases and expenses, and the majority of sales made are zero rated with no VAT chargeable. VAT for farmers is usually a cash flow situation, with a time delay between paying VAT on purchases and recovering that VAT from HMRC. If the farmer is also receiving rent on residential properties then the VAT consequences can be quite complicated as residential rents are exempt from VAT and this in turn could affect the amount of VAT reclaimable from HMRC.

Capital Allowances

Qualifying expenditure for active farming businesses includes expenditure on the cost of: Plant and machinery, its transportation to site, its installation costs and works made to alter land or property to allow installation. Additionally there are a range of allowances as set out in the table.